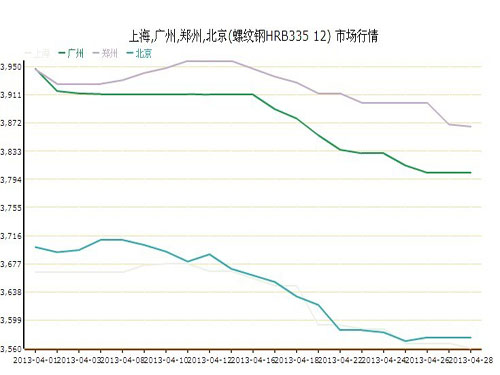

L-Edge Art Blade,Cutting Knife For Art,Pen Knife Craft,Art Pen Knife Chunlei Quntification Co.,Ltd , https://www.hychunleitools.com I. April Market Review “Jinsanyinsi†This is the traditional peak season for the steel market. However, in April this year, the domestic steel market has not significantly improved its supply and demand contradictions. The downstream industry and project steel demand has started slightly, but the release rate is not as fast. It is expected that the steel market will easily fall and rise, and the overall trend will be less volatile. In the first half of the year, the decline in the domestic steel market slowed down, and the prices of the coil and thread markets rose slightly. In mid-May, Baosteel, Wuhan Iron and Steel, and Shougang’s prices were adjusted downwards in May and the preferential rate increased. The domestic economic growth rate was less than expected, and market confidence was not enough. **The electronic market was sharply lower, driving the spot market price to fluctuate. By the end of the 28th, the average price of 20mm tertiary rebars was 3,717 yuan/ton, down by 1 yuan/ton from the previous trading day; the average price of 20mm general plate was 3897 yuan/ton, which was 3 yuan/ton lower than the previous trading day. The average price of 4.75mm HRC was reported at 3753 yuan/ton, which was a decrease of 9 yuan/ton from the previous trading day.

I. April Market Review “Jinsanyinsi†This is the traditional peak season for the steel market. However, in April this year, the domestic steel market has not significantly improved its supply and demand contradictions. The downstream industry and project steel demand has started slightly, but the release rate is not as fast. It is expected that the steel market will easily fall and rise, and the overall trend will be less volatile. In the first half of the year, the decline in the domestic steel market slowed down, and the prices of the coil and thread markets rose slightly. In mid-May, Baosteel, Wuhan Iron and Steel, and Shougang’s prices were adjusted downwards in May and the preferential rate increased. The domestic economic growth rate was less than expected, and market confidence was not enough. **The electronic market was sharply lower, driving the spot market price to fluctuate. By the end of the 28th, the average price of 20mm tertiary rebars was 3,717 yuan/ton, down by 1 yuan/ton from the previous trading day; the average price of 20mm general plate was 3897 yuan/ton, which was 3 yuan/ton lower than the previous trading day. The average price of 4.75mm HRC was reported at 3753 yuan/ton, which was a decrease of 9 yuan/ton from the previous trading day.

Second, the factors affecting the domestic steel market in April:

1. The economic data is less than expected, and the domestic economic recovery is still weak. Domestic GDP in the first quarter increased by 7.7% year-on-year, 0.2% lower than the 7.9% in the fourth quarter of last year, and failed to sustain the recovery. In March, the industrial producer purchase price index PPI fell by 1.9% year-on-year. The CPI of consumer prices rose by 2.1% year-on-year, and inflation expectations were expected to decrease. However, the new stimulus policies are unlikely to be introduced in the short term.

2. The demand for steel products is relatively low, and there are still many uncertainties. From January to March, investment in fixed assets (excluding rural households) increased nominally by 20.9% year-on-year, and the growth rate was unchanged from last year, but it was 0.3 percentage points lower than that in January-February. From January to March, investment in real estate development nationwide increased by 20.2% year-on-year (23.50% in the same period of last year); the area of ​​new housing starts decreased by 2.7% year-on-year (a year-on-year increase of 0.30%), implying that future steel demand is not optimistic. With the promulgation of rules and regulations on real estate around the country, the New Deal has caused improvement in performance and speculative demand to shrink, which may affect long-term sales of homes and new construction.

3, the price of raw materials may fluctuate within a narrow range. In April, iron ore prices oscillated slightly and the coke market continued its downturn. As of the 24th, India's powder ore (63.5% grade) quoted at $139/tonne (CIF), up $1/ton from the end of March. Shanxi secondary metallurgical coke mainstream factory 1180-1230 yuan / ton, compared with the end of March fell 70 yuan / ton. At present, the steel mills are cautious about the purchase of raw materials. In the future, raw material prices may further decline. However, iron ore stocks in domestic major ports are relatively low, and iron ore prices are less likely to fall sharply.

4. High output of steel production. According to data from the National Bureau of Statistics, China's cumulative production of pig iron, crude steel, and steel from January to March was 178.23 million tons, 191.89 million tons, and 245.51 million tons respectively, an increase of 7.60%, 9.10%, and 12.30% over the same period of last year. (3.2%, 2.5%, and 6.5%); in March, the monthly output of pig iron, crude steel, and steel were 61.62 million tons, 66.3 million tons, and 89.61 million tons respectively, an increase of 7.20%, 6.60%, and 9.20% over the same period last year. For the 3.8%, 3.9% and 10.2%), the average daily production was 1,987,700 tons, 2,197,700 tons and 2,890,600 tons respectively. At present, domestic steel mills have not yet experienced large-scale production cuts and overhauls. The control of production by some steel companies cannot relieve the pressure on overall resources.

5. Slow decline in steel social stocks. As of April 19, the five major steel stocks in major cities nationwide were 20,842,500 tons, which was 470,000 tons less than the previous week. At present, social stocks have declined for 5 consecutive weeks, but the social inventory of hot stocks has been increasing, and the cold rolling and medium board have had a limited decline. At present, the total amount of rebar inventories in major cities across the country is 9,951,100 tons, a decrease of 327,200 tons from the previous week and an increase of 2,303,600 tons from the same period of last year; the inventory of wire rods is 2,831,200 tons, a decrease of 122,400 tons from last week; The total amount was 4,825,500 tons, an increase of 41,400 tons from the previous week; the total amount of cold-rolled inventories was 1,630,700 tons, which was a decrease of 46,400 tons compared with the previous week; the total stock of medium plates was 1,600.25 tons, a decrease of 15,300 yuan from the previous week. Ton. According to the data from the China Iron and Steel Association, at the end of April, the steel stocks of the steel association members and companies were 13.7334 million tons, which was 0.2% higher than the contract price in the end of the decade. The contract organization of steel companies still faced greater pressure.

6, steel prices cycle or will end. In May, the factory prices of Baosteel's hot-rolled, cold-rolled and other mainstream varieties remained unchanged, but the order preference margin increased. The price of Wuhan Iron and Steel Panel was lowered by RMB 100-240/ton, that of Anshan Iron & Steel was lowered by RMB 100-150/ton, that of Shougang Group by 150 yuan/ton, and that of Hegang by RMB 200-250/ton, reflecting the steel mills' future market It is still not optimistic.

Third, the market trend forecast in May In short, in April, gold, crude oil and other commodity markets have experienced a sharp decline, which will usher in a rebound process in the later period; while the country’s intention to expand domestic consumption in the second quarter, the intention to stimulate investment growth is very obvious; Therefore, the demand side of the steel market may continue to improve. In May, the market is facing the pressure of gradual decline in demand and further downward pressure on costs. However, implementation regulations for urbanization planning have not yet been introduced. There are many uncertainties affecting economic operation, although steel is used. The industry is already in peak season, but demand is still tepid. The area of ​​new construction of housing construction industry is down, and the overall manufacturing industry is still sluggish. In terms of inventory, the production of steel may decline in the later period, but the absolute amount will remain high; steel mills and society Slow decline in stocks; leading steel mills cut prices in May, the steel mills price increase cycle may be over, in general, the domestic steel market supply and demand in the latter part of the contradiction is still prominent, in May prices will fluctuate lower.